Dry powder lines

There’s a lot going on in the investing world outside the public markets. Some observations, and questions from the shift to Privates.

I’ve been mostly talking about public markets and investing here on the Atomic Investor. But there’s a lot going on in the investing world away from the eye of the public markets that you do not want to miss out on. For context, Private markets have quadrupled in size over the last decade, growing from roughly $2 TRILLION in assets in 2010 to almost $8 TRILLION in 2021.

But first...

A quick recap (of what you already know)

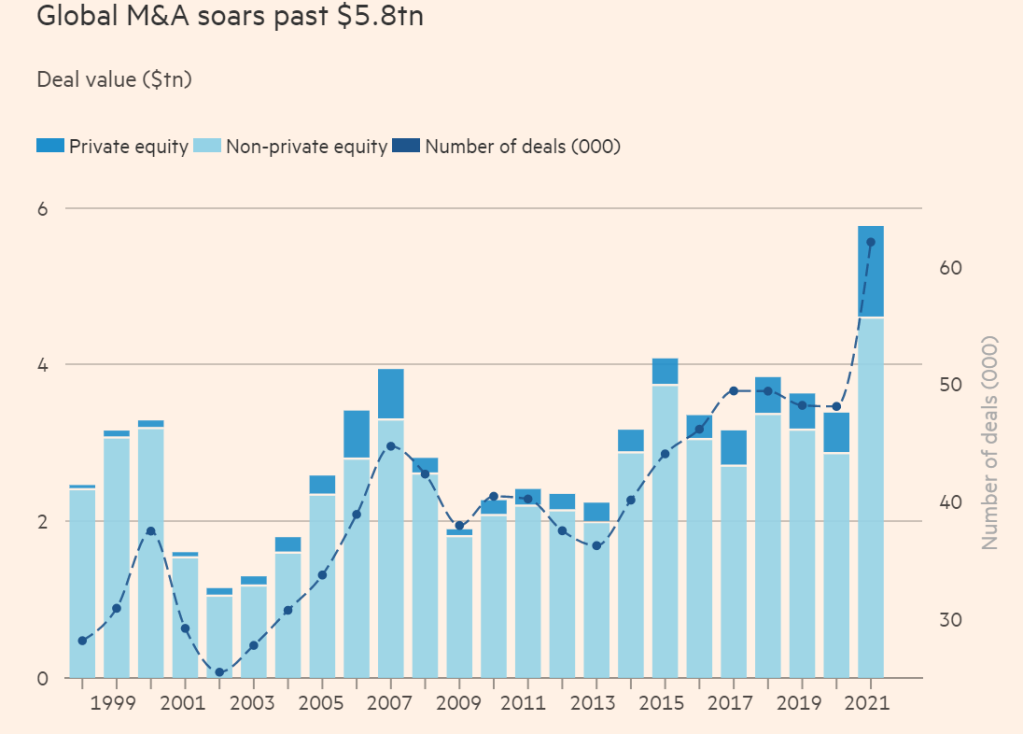

2021 was a remarkable year in finance and capital markets. If you’re a banker, an investor, or a consultant working in the industry, you know what I’m talking about. For the rest of the world, here’s some numbers.

The M&A market generated $5.8 TRILLION worth of deals and transactions this year (64% growth YoY). Companies raised a record $12.1 TRLLION of capital. We saw a swath of IPOs, stock issuances, bonds and loans being issued to recapitalise firms, fund takeovers and help investors cash out.

Ultra loose financial conditions globally created a goldilocks environment for borrowers, investors and dealmakers. Falling long-term yields drove borrowers to lock-in long-term funding cheaply, whereas investors underwrote whatever yield that came their way in the negative real-yield (and for a large part of the developed world, nominal yields as well) environment we have been in. 👇 🤌

Private equity and SPACs have led a significant proportion of those deals. Some $1.1 TRILLION of bonds have been raised by PEs alone to fund the massive amount of leveraged buyouts during 2020-2021.

“We didn’t just break the record, we crushed the record. It wasn’t even close.” - Jim Cooney, head of equity capital markets for the Americas at Bank of America.

Here’s a head-spinning number for you:

Despite all the capital being deployed recently, globally PEs still had a dry-powder pile (the capital that has been committed but not invested) of $2.9 TRILLION. In 2021 alone, a total of $780 BILLION of capital was raised that is yet to be deployed, which takes the total dry-powder mountain to roughly $3.7 TRILLION.

Makes one wonder that it takes a LOT to go from ‘rates being low’ to a ‘trillion dollars being piled onto the uncommitted capital.

Why now? And what is going on?

The hunt for yield

We’ve known about the structural downtrend in long-term rates for some time now. A multitude of factors, some of them being an ageing population, technological advancements (contentious, but yeah) and the ever expanding balance sheets of global central banks are at the centre-stage of this secular trend.

The fixed income asset class is a substantial part of retail and institutional portfolios. Think about all the retirement portfolios, pension funds and endowments with an investment horizon of 20 years or more. At the end of 2020, global pension fund held assets amounting to almost $56tn. For an ageing population that is living for much longer, you need considerably higher returns to match these pension liabilities (the retirement money owed).

Falling rates, with a bulk of those in negative territory means you would expect even lower future returns from the asset class.

The 2008 crisis was what really set this ‘hunt for yield’ in motion, but the recent shock really pushed long-term investors (like pension funds and endowments) further out the risk-curve in search for higher long term returns, as both cost of capital and expected returns fell sharply. (cheap money = lower cost of capital, higher valuations today = lower expected returns in the future)

The shift to Privates

Higher equity valuations and lower yields is like a double-whammy for the 60/40 portfolio. Long-term return expectations of a 60/40 (60% Equities and 40% Bonds) portfolio are now as low as 2%, with the long-term average being nearly 5%, according to AQR.

Low returns and a steadily growing alternative asset management industry led the shift to privates gradually at the start of the century. But ultra low rates, easy leverage and even lower return expectations has now accelerated this allocation to private strategies. Once could say it might have shifted the focus substantially from public equities to private markets, which are now mainstays of these long-term portfolios.

Such a shift in the markets is hard to view in isolation, and there’s ought to be some adjacent first and second order effects emanating from this. Here’s a few of them with some open-ended questions to ponder upon.

Leverage fueled party:

Leverage is a core feature of all private strategies. Easy credit and increasing private transactions has allowed managers to pile on more leverage than ever on the target company balance sheets. All this illiquid and lower rated debt should be cause of concern, especially now. When the liquidity spigot normalises and rates go up, what happens to all that leverage in the system?

Companies staying private for longer:

PEs and VC’s ratcheting up their fund velocity has allowed both young and established private companies to tap into this ever increasing and ever willing pool of capital. Although it feels like we’ve seen tons of IPOs recently, the average age of companies going public is increasing. Companies are staying private for longer, and going public is turning into an exit for private shareholders, than an important milestone for companies and founders. What implications does this have for public market equities? And how much more value is left for public market investors when these companies come to market at sky-high valuations?

More dry powder than targets:

PE and VC funds are raising funds faster than ever. That pile of dry powder, the unallocated capital is as high as it has ever been. And now, all that capital is chasing a limited number of targets, which is pushing up the valuations across the board. According to FT, the average premium paid (the price paid for the target company) on listed company buyouts was close to its 2003 highs - over 45%. We’ve seen this story play out before in the public markets. What form does this spiral of multiple compression take in the private markets when this eventually normalises and buyers are scant for businesses with overleveraged balance sheets?

The growth in privates is looks set to continue. Niches like private credit and infrastructure are attracting higher allocations to eke out whatever yield there is. This hunt for yield has ballooned private credit AUM to more than $400bn. Strategies like growth equity (a private strategy that invests in established but much riskier businesses) are now growing at double digit CAGRs.

One could expect the dealmaking to continue, as the unallocated capital tries to find its next target and invested capital is returned back to the LPs, eventually to be recycled back in again.

We might as well get used to seeing these dry powder lines for much, much longer.

Until next time,

The Atomic Investor