No L for Luxury

The Luxury market has shown resilience and strength in an uncertain macro environment. Doesn’t look like there will be any Ls for Luxury in the short term.

Its been a tough year so far. Rising interest rates have caught both businesses and consumers off guard. Inflation is burning a hole in everyone’s pocket on top of that. Most sectors are feeling the heat in an environment as they face the double whammy of demand slowing down and higher input costs. It should not be a surprise to see the markets pulling back as expectations and discount rates get reset and the R word starts getting thrown around with an increasing frequency.

In all this doom and gloom surrounding the markets and the economy, there is one sector that has almost looked like a canary in a coal mine.

No L for Luxury

Luxury has been one of those sectors that came out stronger and more resilient from the pandemic in 2020. After contracting during the tough year, it came roaring back in 2021 with a 15% growth, taking its overall market size to $1.14 trillion.

Personal luxury goods, cars, hospitality and wines & spirits makes up for more than 80% of the market and all of these sectors have compounded significant value over the last decade or so.

The strength it has shown this year, a year shrouded in uncertainties, has been quite fascinating. The global personal luxury goods market is expected to grow by more than 22% this year alone, which is a chunky step above its long-term trend growth of 6-8% annually.

Here are a few interesting trends that might help explain luxury’s resilience.

The world at the top is getting richer

The global wealth share of the top 1% has steadily crept up and now stands at 45.6% in 2021, moving up from 43.9% in 2019. This is important as the High Net Worth and the Ultra High Net Worth individuals contribute to more than 40% of the global luxury sales (which was 35% in 2018). As the wealthiest at the top keep getting wealthier and increasingly contribute even more to the overall luxury market, economic recessions or downturns are likely to have a more subdued impact on the luxury market.

The China growth story

The Chinese expanding middle class prosperity has been a phenomenal growth story playing out over the last three decades. Median wealth per adult in China has gone from $3100 in 2000 to USD26,700 in 2022 with an annual growth rate of almost 11%.

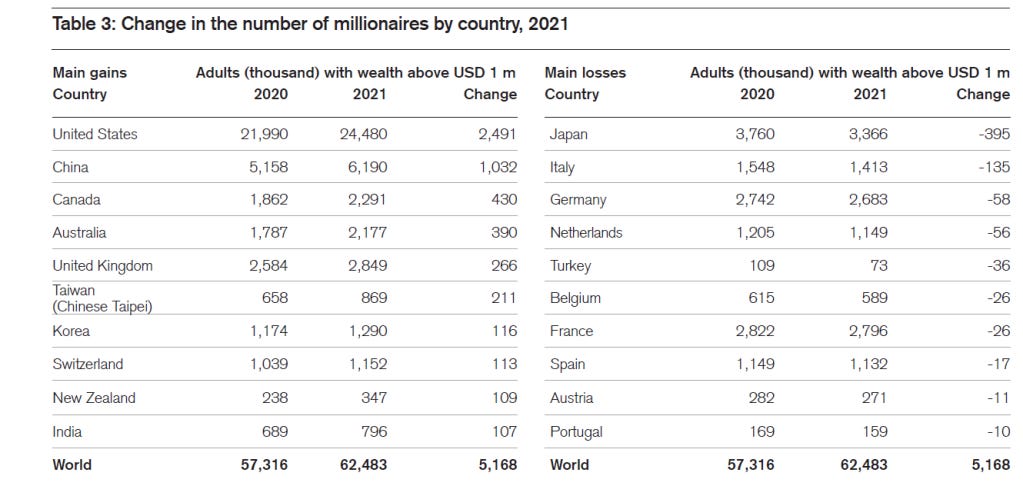

The number of millionaires in the country have also climbed the charts, and now account for 10% of the world’s total (with the U.S having a 40% share).

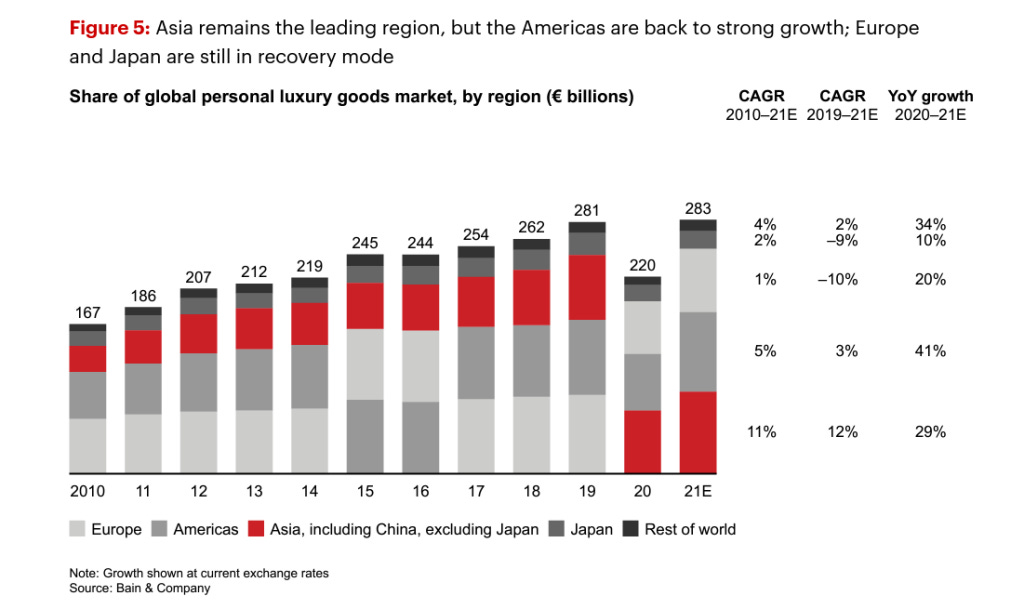

An expanding wealth of the middle class and the rich meant more travelling and spending on luxury goods and experiences. This propensity to spend on luxury also attracted the largest luxury brands to China and the region now accounts for more than 30% of the global personal luxury goods market.

Even with a strict and prolonged lockdown, demand from China has held stable (if not growing at double digits like other regions). The eventual full reopening of the country should further act as a strong tailwind for the global luxury market as the Chinese start fully travelling again.

Its truly Veblen

Luxury goods are truly veblen in nature. The more expensive the item is, the more attractive it becomes in the luxury category. If you’re in the HNW or UHNW bracket and are given a few items to choose from, you’re more likely to buy the most expensive brand out of those. At that level, the price is a signal of your purchasing power and your net worth.

Even an inflationary environment where luxury brands push the prices up to counter rising costs is unlikely to impact your decision to buy that item (until a certain price point of course). Therefore, luxury brands have structural pricing power and can pass on increasing costs easily without consumers substituting to other cheaper goods.

The market is more consolidated than before

The market has been consolidating over the last decade as brand houses become house of brands. LVMH, the worlds largest luxury conglomerate now owns 75 “maisons” or workers under one umbrella. It acquired Tiffany’s in the U.S in 2020 to strengthen its presence in the world’s largest luxury market.

The Kering group owns a multitude of brands such as Gucci, Bottega Veneta and Yves Saint Laurent and Balenciaga.

The Estee Lauder group recently acquired Tom Ford for $2.8bn and already owns a range of beauty brands in the U.S.

A portfolio of iconic brands allows companies to leverage synergies in manufacturing and distribution by using shared resources and channels. A consolidated market also lends additional pricing power to brand conglomerates and gives them more control over the supply chains.

Brands are getting better at telling a story

Luxury brands have always been good at captivating their customers with their designs. Now, the biggest of brands are getting even better at weaving narratives around the society and sustainability to target different customer cohorts.

Their marketing campaigns include the most loved and the most iconic personalities of the world with billions of followers. They reach an ever increasing number of people via social media, influencers, celebrities and creators attracting customers from the range of generations and demographics that were not easily penetrable. Like this thing of beauty released right before the World Cup for example, which racked up more than 72 million likes within days on Instagram.

By investing more in the communities from where they source their materials and manufacture their products, these brands can differentiate themselves from other cheaper fast fashion houses of the world.

Investing in luxury

Publicly listed luxury stocks are a decent way to get some exposure to the global luxury market which is expected to grow by 5-10% annually for the next few years.

The largest of them all by market cap, LVMH, is my pick of the bunch. LVMH is present in the largest luxury segments - Fashion & Leather goods, Wine & Spirits, Watches & Jewelry and Perfumes and Beauty and has almost doubled its revenues from 2017 levels.

The stock has outperformed its local benchmark by a country mile, and has been the best performer in its peer group this year and over the last 5 years.

Fundamentally, things look a lot better than 5 years ago. LVMH has a 20bn euros revenue run rate per quarter now from 10bn euros back in 2017. Operating margins have improved from 19% in 2017 to 28% in Q3 2022 (a higher contribution by high margin Watches & Jewelry segment via the Tiffany acquisition is already reaping its rewards).

On top of all that, the company generates more than 13bn euros of free cash flows paying 12 euros/share in dividends which have grown at a CAGR of 15% on average over a 5 year period, going back more than 20 years.

Kering group, the parent group owing the popular Gucci brand, and Hermes, the famous creator of Birkin bags and scarves, are two other stocks that have delivered a robust revenue growth and fairly healthy margins.

Other luxury stocks such as Moncler, Richmont and Ferrari have been impressive too, outperforming their local stock markets over the last 5 years.

Both luxury stocks and the market have shown strength and resilience in tough macro environments. As long as the key drivers do not show weakness, which I do not think they will in the near term, there might not be any big Ls for luxury anytime soon.

Until next time,

The Atomic Investor