Not a $COIN flip

Coinbase Q2 earnings and why I’m bullish.

Inflection points are easy to spot in hindsight, but hard to predict ex-ante. Coinbase, one of the world's largest cryptocurrency exchanges and platforms, went public in April this year. As I mentioned in one of my earlier posts, this was huge event for Crypto. The first ever listing in the space in the largest financial market in the world gave it a sheen of legitimacy to it. It changed the entire narrative. Even BTC rallied to all time highs of $63,000 that day. While we cannot declare this as an inflection point yet, if there ever will be one, in hindsight this event could be a contender for it.

$COIN declared its first earnings as a public company this week, blowing expectations out of the water.

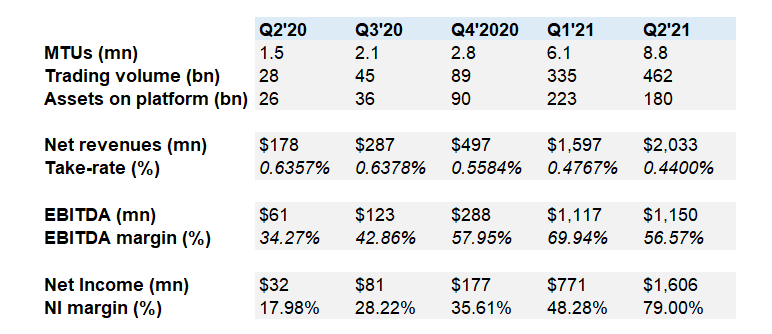

Monthly transacting users (MTUs) climbed to 8.8mn from 1.5mn in Q2 2020 and 6.1mn in Q1 2021. (+486% YoY)

Trading volumes reached $462bn from $89bn in Q2 2020 and $335bn in Q1 2021. (+419% YoY)

Net Revenues made all the headlines, with a 1000% jump from Q2 2020, reaching $2bn

EBITDA reached $1.15bn from $61mn a year ago with net income climbing to a staggering $1.6bn

$COIN makes almost all of its revenues from transaction fees, so a quick back of the envelope calculation gives you a take-rate of 43 basis points (Net revenues/total volume). This means for every $100 of crypto assets traded on the platform, $COIN makes 43 cents. This is much higher than other trading exchanges like NASDAQ, CME and ICE.

What to make of all this?

With so much going on in the crypto space, $COIN could be a wonderful stock to own. Crypto assets are now slowly reaching acceptance in not just retail but institutional portfolios. Institutional clients now make up 68% of all the volume (from 64% previously) on Coinbase, which is likely to increase even further as it onboards bigger institutions. While this would lower the blended take-rate in the long-run, it allows the company to reach scale and execute trades better at the same time.

Exchanges are all about scale and Coinbase needs institutional investors trading in millions (and maybe billions) to make up that volume. The CEO Brian Armstrong mentioned that 10% of top 100 hedge funds in the U.S are now its customers using the Coinbase Institutional platform. The company openly says it wants to provide the cheapest access to crypto assets. And for that reason, it offers its institutional clients access to crypto for just 3 basis points (compared to retail tx fee of 1.26%). It has other monetisation avenues for institutional clients like custody and prime lending which are likely to grow from here.

"We do not compete on fees. Instead of focusing on being the lowest priced platform, we focus on providing the most value to customers through our custody, our security & storage in addition to trade execution."

What I like

The nature of the business

The innate nature of the business provides it considerable operating leverage. Incremental costs to serve new customers get lower as the business reaches scale and we are already seeing that in action in its margins.

Antifragility

The company admitted that it was a volatile quarter for crypto and put that as one of the reasons for the fantastic results. Antifragility (it gains from volatility) is an important characteristic of the business. While volatility is hard to predict, its impact on Coinbase is clear.

Security

It has also handled platform security pretty well so far, one of the most important aspects when it comes to attracting larger clients. Just this week we saw assets worth $600mn being hacked from Poly Network (most of which were returned later)

Regulation as a competitive advantage

While most crypto startups focus on the technology and the business first, a focus on regulation was always front and centre at Coinbase. Brian Armstrong was in constant touch with the SEC and various other regulators in the years leading to its IPO to stay ahead of any upcoming changes to regulations in the countries it operates in. Binance, a key competitor, was recently banned in the UK which clearly shows that the hammer could drop at literally any time.

Here's another thread on $COIN's Q2 results, with more insights into their customers and fees.

Not a coin flip

This is a classic 'picks and shovels' play. While I do not know what BTC is likely to be worth or where ETH is likely to be, growth in crypto trading, DeFi, applications and ownership would benefit $COIN as it becomes the go-to platform to have access to crypto assets. $COIN is an exposure to crypto without owning any directly.

There's a slate of Bitcoin ETFs in contention to be approved by the SEC. This would drive more institutions and market participants towards the space. ETF flows would be a massive tailwind for both BTC and ETH, adding more volume to the crypto markets.

It trades at a premium to its peers both an P/E and EV/EBITDA basis but has outperformed everyone by a mile on earnings and EBITDA growth.

Take rates and user growth are the key metrics to watch out for. Retail is still a big chunk of its business.

I'm still bullish on this one. This is not a coin flip by any means.

Leaving you with a tweet that should excite anyone interested in $COIN

Until next time,

The Atomic Investor