Pipes to Bits: A tale of two infrastructure booms

The echoes of the dotcom era's infra. buildout are reverberating through today's AI revolution, but with a twist - while the investment scale is comparable, the financials tell a more complex story

Remember when telecommunications giants were the backbone builders of the digital age? In 2000, companies like Cisco, Lucent, and Nortel commanded about 13% of market-wide capital spending. Fast forward to today, and NVIDIA's data center revenues are projected to capture an even larger 17% share by 2026.

It's a striking parallel, but one that masks fundamental differences in the underlying business dynamics.

The Great Infrastructure Flip

The most telling crossover is visible in Microsoft's capital expenditure trajectory. The once-quintessential "asset-light" enterprise software company now spends more relative to its sales than Verizon, with its capex/sales ratio surging to 25% while the telecom giant hovers around 13%.

This dramatic role reversal illustrates how Big Tech has evolved from being merely a tenant of digital infrastructure to becoming its master architect.

Here are how the numbers stacked up in 2024:

*Note: All figures in billions of dollars. Operating costs include cash operating expenses, software, depreciation and electricity

The spending spree shows no signs of abating. Meta, Amazon, and Alphabet have all indicated that their capital expenditure will be higher in 2025 than in 2024. Goldman Sachs expects hyperscaler capex to reach $264 billion this year before rising to nearly $300 billion the next.

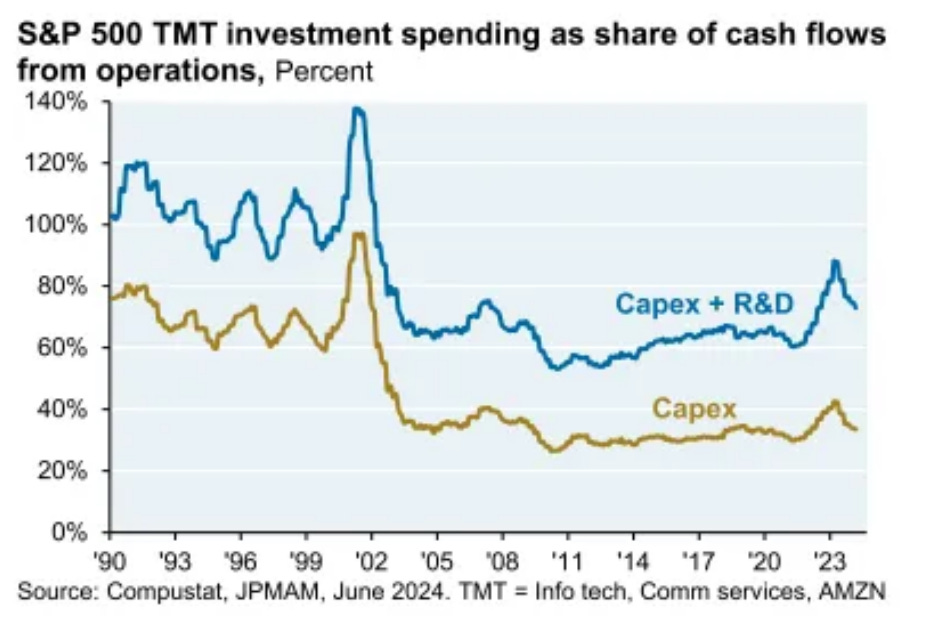

But here's where history diverges. Unlike the telecom companies of the dotcom era, today's tech giants are generating enormous free cash flows while making these investments. Their capex + R&D to operating cash flow ratios remain manageable, suggesting these investments are more sustainable than the debt-fueled expansion of the past.

Another key differential might lie in the shorter payback periods for AI investments and the continued robust growth of core businesses. Microsoft, Meta, and Alphabet maintain capex and R&D spending at 30-45% of revenues while growing their fundamental operations - a stark contrast to the telecom boom's aftermath.

But this also creates an interesting paradox: while these companies have the financial strength to fund massive infrastructure investments, unlike their telecom predecessors, the sustainability of this spending trajectory is becoming a key investor concern.

The Depreciation Conundrum

While these tech giants still generate substantial free cash flow even after their massive AI investments, free cash flow (operating cash flow less capital expenditures) across major tech companies is flat to declining. This matters - during previous cash flow downturns (like 2021-2022), these stocks significantly underperformed the market, with Microsoft being the sole exception.

Adding to the complexity is the opacity around how these investments will be depreciated. Ravi Gomatam of Zion Research Group points out that modeling future depreciation at big tech companies is highly complex. Data center investments comprise multiple components - servers, infrastructure, buildings - each potentially depreciated at different rates. The rapid pace of AI innovation adds another layer of uncertainty, as equipment obsolescence could trigger unexpected writedowns.

The gap between capex to revenue and depreciation to revenue is 11%, with the former growing much faster for now. But that gap when eventually hits the income statement the operating margins could take a considerable hit.

The historical cautionary tale of Corning's fiber optic business serves as a sobering reminder - after peaking at $4 billion in 2000, it took 18 years to recover to those revenue levels in nominal terms, and in real terms, they're still below those peaks.

Looking ahead

As we witness the next wave of AI infrastructure expansion, with hyperscalers estimated to have spent $222 billion on AI chips and data center infrastructure in 2024, the investor community stands at a crossroads. The debate is now evolving in real-time between scaling laws versus inference efficiency and whether capital intensity will remain the moat it appears to be today. The focus will likely shift from AI hype to harder metrics - investment levels, depreciation policies, and most crucially, cash flow generation.

"Investment, depreciation and cash, and not just AI hype, will matter for tech investors this year."

The telcos built the information superhighway, but today's tech giants are building something potentially more transformative - the infrastructure layer that will power the next generation of computing. The question isn't whether they can afford to build it - it's whether they can afford not to. And the answer might lie not in the amount of capital deployed, but in how effectively it translates into new sustainable competitive advantages.

It remains to be seen is whether this infrastructure boom will follow a different path than its predecessor, or if, like all cycles, it will eventually find its own equilibrium.

What is even more likely is the emergence of new winners (and eventually losers) in the next phases of the AI cycle. More on that in the upcoming pieces.

Until next time,

The Atomic Investor