Somewhere to hide

While the markets come to terms with higher inflation, investors are looking for somewhere to hide and seek some shelter for their savings.

A sustained period of high inflation can be tricky. If you invest your savings, inflation can have a “one-two-punch” of the falling value of your invested savings (via financial markets, decreasing purchasing power) and higher discretionary and non-discretionary costs.

The U.S CPI print came unexpectedly high (again) yesterday with a 1% MoM and 8.6% YoY increase. The markets continued their sell-off with yields climbing higher with the expectations continuously being reset. Most asset classes seem to be in a precarious situation as the probabilities of a recession inch higher. Equities are under pressure as companies deal with margin pressures, higher wages, higher cost of capital and basically reversing everything that pushed the stock prices higher in the last couple of years. Bonds are under the worst drawdown in decades as central banks take back the free-money spigot and rein in higher inflation. Therefore quite naturally, investors have been increasingly looking at somewhere to hide. The unloved asset classes of the forgotten past - Resources and commodities are making a comeback as the market seeks protection during this period of high inflation. Something that is a very new new thing for a lot of us.

A complete turnaround

After a dreadful run for a decade or so, commodities made a spectacular turnaround in late 2020 when the alarms of supply chains breaking down went off. What happened after (soaring demand fueled by free money and the Russian invasion) created a perfect storm for commodities like energy, food and metals globally.

Commodity funds are up more than 60% over the last year with oil, natural gas and food prices up a lot more than that. This temporary, transitory, supply driven price increases have turned into structural price increases all over the place, with higher energy and raw material costs feeding into higher consumer prices, wage increases (due to labour shortages) and so on.

A long time coming

The ex-post narrative going around says that this was a long time coming. Central banks waited for too long to come out of their ‘transitory’ stupor to end the QE programs. Supply chains are still struggling to cope up with Covid lockdowns in China and higher freight costs. The war between Russia and Ukraine, which are the one of largest suppliers and energy and food to the world, is not getting resolved anytime soon. Since central banks cannot control the supply side of the equation, the consensus view is they will try to rein in the other side of the equation and bring down demand via taking liquidity out of the system and raising rates.

But the commodity shortages go way back. According to GMO, the world consumes 40% more commodities than it did 15 years ago, but capex levels to produce those commodities are at 15-year lows. Underinvestment in supply driven by de-investment in production, more stringent environmental checks to approve projects and falling commodity prices over the last decade led to falling production capacities, which are now at levels unable to cope up with the current demand.

Here’s an explanation:

“One commonly expressed view is that the clean energy transition will displace fossil fuel demand, leading to lower prices. The analyses that form this view, unfortunately, completely ignore the supply side of the equation. If you don’t invest hundreds of billions of dollars in capex each year, for example, you see depletion rates of 6-8% for conventional oil wells. Shale depletion rates are much, much higher, averaging around 70% by the end of the first year. If fossil fuel companies see demand disruption, they’re bound to cut capex, leading to a significant reduction in supply and perhaps, counterintuitively, higher prices”

Is it time?

Given the recent outperformance of energy and commodities, and the higher expected inflation and lower supplies scenario getting closer to becoming the “base case”, the asset class is generating quite a lot of interest. One might wonder if now’s the right time to get serious about allocating some capital here.

GMO, in the same letter, opined that valuations and free cash flow yields for the sector are still attractive and makes a case for investing in the asset class.

But that might not be compelling enough. Energy and commodities are highly cyclical with multiple booms and bust cycles in the past. That means entry and exit points of your investments are important, something that to get right is extremely hard not just for us Atomic Investors, but also for a lot of professionals.

Here’s a few things that you might need to look out for before you shell out your capital:

Inflation hedging capabilities and return expectations

If you’re investing in commodities/resources as an inflation hedge it is important to understand how well could they be expected to perform under different environments. The three major expected outcomes -

Prices increase/inflation is accelerating,

Prices remain where they are/inflation reaches a higher steady state and

Prices decrease/inflation is under control and falling

and their respective likelihoods could determine how well these stocks or asset classes perform. They’ve rallied from their lows of 2020 and outperformed due to an unexpected supply shock, sudden spike in demand and compressed long-term valuations, leading to a reallocation towards these sectors from the recent winners in tech and growth.

According to Meketa, the inflation hedging capabilities of natural resources (especially energy) have reduced as compared to previous inflationary periods due to a slow shift away from oil and transition towards other forms of energy. However, given that there are still no complete substitutes for it, it can still provide some inflation protection. They lay down three conditions that when aligned provide an environment for this asset class to work:

Low/no substitutes and negative supply shock in an inflationary environment is what we witnessed in the last two years, therefore creating a solid ground for this to work.

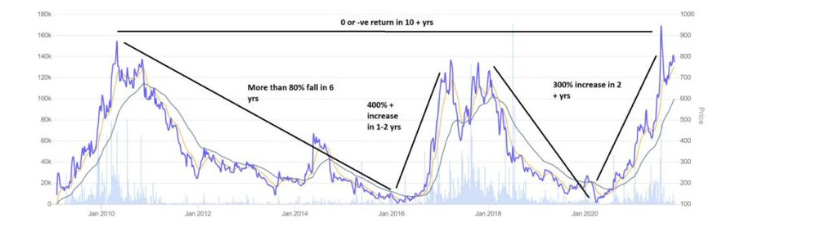

Investing in cyclical asset classes

Cyclical investments are hard. Your returns can vary extremely based on what part of the cycle you enter and exit your investments. Cyclical asset classes could get you multi-bagger returns if you get in close to the lows and you could also 80-90% of your capital if you get in close to the top.

The best time to invest is therefore when the performance of these business in terms of revenues/margins are at their lows and the worst time could be at the other end, when the performance is at their highs. Its almost impossible to pick the exact bottom, but you at least need the right entry directionally (when the commodity prices are on the way up). Your risk-reward at that point in time would help you get a better decision.

Time horizon and risk apetite

This goes in hand with the sections above and probably the most important thing to consider before you invest here. Your time horizon (short-medium-long term) is not only impacted by your risk apetite and the ability to take riskbut is also dictated by by the duration of current interest rates/commodities/market cycle and the point where you are at the time of investment. Given the volatile nature of this asset class, the appropriate horizon is rarely long-term (decades) and might be rather just years.

Know where you are, know your time horizon and know your risk apetite and the ability to take on risk.

Starting point: Marginal capital or reallocation

Your starting point might decide how you might want to go about your investment. If its marginal capital you’re allocating (additional capital outside what you have already invested) you would normally be looking at risk-adjusted expected returns and your opportunity costs in the form of cash, stocks, fixed income, other assets and their expected returns.

If you’re reallocating from your existing portfolio (selling something and allocating here) you would be looking at your current gains of what your selling, expected relative performance between what you’re selling and what you're buying and how this reallocation could impact your portfolio’s performance.

Execution

Ideas and strategies are only one part of the puzzle. Execution is how you implement them. Based on the type of investor you are, and the amount of risk and resources you are willing to afford, you could use different types of products to allocate your capital. Here’s a few of them:

Futures: Some investors prefer to position themselves via commodity futures or options. Given that you need to place collateral and you invest on margin, this strategy comes with high risk, constant monitoring of positions and high volatility.

Stocks: One could try investing in commodity or resources stocks from the energy, metals, agriculture subsectors. Stock-picking is never easy and you need an understanding of sector the company operates in, the intrinsic issues if that company and how it is positioned to perform in this commodity cycle.

ETFs and Funds: The least risky way out of the three, by way of diversification,lower costs, lower volatility. There are broad based diversified commodity funds like ICOM, PDBC or specific sub sector funds holding food, metals and energy stocks and futures that you could allocate to. Here it is important to not only pick the right time, but also the right fund.

While the markets prepare for a sustained period of high inflation and assess the wide range of outcomes, you might as well seek some shelter for your savings in the meantime.

Until next time,

The Atomic Investor