Private Equity's new reality

Two sets of opinions on PE valuations and outlook from the opposite ends of the spectrum.

I got my hands on a couple of interesting reads on PE this weekend. Two different sets of opinions from the opposite sides of the spectrum on the never ending debate around PE valuations and how they drive returns. As I opined in Upping the stakes , PE’s phenomenal growth and returns command extra scrutiny and attract both believers and naysayers. Therefore, its normal to have a difference in opinion (and back it up with verifiable data whenever you can). Not just for PE but any asset class in general.

The first one, a note on PE fundamentals by Verdad Research argues that a correction in PE valuations is warranted.

They analysed a sample of publicly listed PE/VC backed companies (30%+ sponsor owned) or PE backed businesses with debt trading in public markets. The sample represents $750bn in value (around 6-7% of PE AUM) and had a 40% weight towards the tech sector.

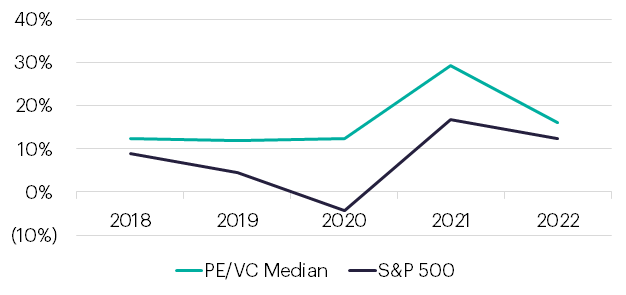

The sample had a much better revenue growth than the S&P 500 (used to benchmark against public market equities), compounding at 16% vs 7% for the S&P.

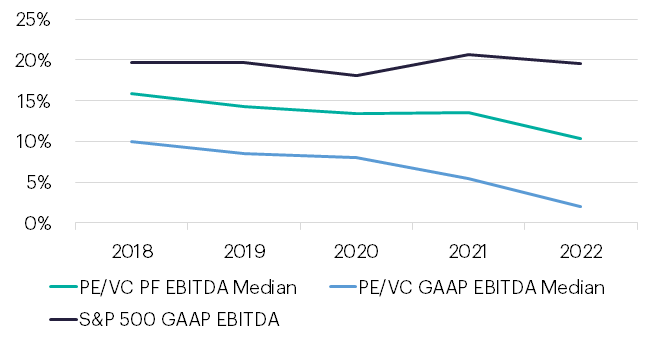

However, EBITDA margins were not as attractive for the PE/VC backed company set.

To support their opinion on PE valuations being too high and could be in for a correction, they argue that PE backed businesses are highly leveraged (8.8x on GAAP EBITDA and 4.9x on pro-forma EBITDA vs 1.7x for the S&P) and have much higher interest costs (43% of EBITDA vs 7% for the S&P 500).

Given the surging cost of debt for private companies (10-12% floating rate loans on average) and a challenging growth environment, they should be valued at a much lower multiple than what they are at right now.

They end at a cautious note (a part of which stood out and I’ll come back to later),

“Resolving these challenges will be difficult. Growth seems more challenging in a wobbly economy, and the tailwind of rising multiples has disappeared. Private equity sponsors will likely need to have difficult conversations with their lenders and focus on operational execution to manage costs as they navigate a less friendly macro environment.”

The second read was almost like a counter-argument to some of the quantitative data presented above.

StepStone Group published a short piece on PE valuations and return attribution, backed by an analysis of a much larger proprietary private company dataset.

One of the recurring arguments against PE returns is that easy market conditions and low rates have driven multiples higher pushing investment IRRs up, and now in an environment when that is unlikely to work, PE returns would falter.

According to this piece of analysis, revenue growth and margin expansion has contributed to 300% more unlevered value creation than multiple expansion in this cycle since 2015.

Then, as compared to the S&P 500, revenues for PE backed companies grew 4.1% faster on average, which makes you question if PE multiples should be expected to move in-step with public markets, especially the S&P 500.

Their analysis of return attributions for the cycle since 2015 suggests revenue growth and margin expansion have been key value drivers for PE backed companies. Quite the contrary to arguments presented against the industry.

Both reports have diverging opinions but have an overarching theme that underlies Private Equity’s new reality. Here are some my key takeaways:

While multiples and leverage have acted as tailwinds, the real value has been, and given where market conditions are, will increasingly be created by operational improvements and strategy reorgs which drive revenue growth and margin expansion for the business. Both Verdad and StepStone allude to this new environment for private market investors.

PEs need real business operators/advisors, not just dealmakers, to ensure fundamental improvements that warrant a higher future multiple and put the business on the growth path.

This might make it harder for smaller, emerging GPs to compete with the big guys, who have access to the resources and the experience needed to drive those fundamental business changes. We’re already seeing it play out as allocations are increasingly being directed towards larger funds with a track record.

Volatile market conditions have a larger impact on capital markets (making them hard to navigate), than the actual value creation levers for PE. Deals and M&As are harder now, but just getting them over the line wouldn’t ensure success as the leverage/multiple expansion levers become ineffective. Operating excellence and a business strategy aligned to your growth plans and targets is key.

Its quite easy to make the data fit your story. Public market multiples are a good starting point to see the range of entry/exit multiples you could expect, but valuing PE backed businesses using them is not that straightforward.

Private companies have a different fundamental and risk profile. Public markets are driven a lot more by sentiments and narratives, where a company’s shares change hands by the second. Private deals incorporate information public market investors are unlikely to have access to, and are priced based on what the business could like in a few years. PE multiples have come down and might continue to do so, but they move more in tandem with market conditions like deal flow, financing conditions and buyer/seller expectations, which might be directionally similar to public markets but they do have to be equal in absolute terms.

There would always be opinions and arguments at both sides of the spectrum, but its important to take both sets of views under consideration to keep your biases in check. Also, at times even though they’re aiming to reach opposing conclusions, they might give an affirmation on a different theme or an idea altogether.

In this case, it is the PE’s new reality.

Until next time,

The Atomic Investor