Real Assets get real

The changing nature of infrastructure - from low risk stable asset class to a dynamic higher return investment is driving consolidation amongst GPs to combine resources and expertise to achieve scale.

Forgive me for repeating what others have stated numerous times already, but 2023 was another tough year for Private Equity dealmakers. As per the annual industry reports, total deal value continued to fall and was down 29% in the US and 26.5% in Europe YoY. The apparent drought in investment exits, now down roughly 25% both in the U.S and Europe, has slowed things down considerably. While the long awaited rebound in dealmaking might not have arrived just yet, M&A activity between Fund Managers has started 2024 on a cheerier note for the industry.

To kick things off, BlackRock, the public markets asset management behemoth with more than $10tn in AUM bought Global Infrastructure Partners (GIP) in a deal valued at $12.5bn, adding more than $100bn in Infrastructure assets to its private markets business. Then General Atlantic, the Tech focused Growth Equity investor bought Actis, a specialist sustainable infrastructure asset manager, to expand into Real Assets - investments backed by physical assets such as real estate, power and energy related assets, digital infrastructure (data centres, mobile towers, fibre networks) and transport.

These two and other notable deals last year like CVC-DIF and Bridgepoint-ECP strongly highlight the very evident shift away from the traditional PE business. As I mentioned in Not Just PE Anymore, a diversified stable base of fee earnings is the north star for asset managers that has been guiding their recent activity in the markets in a bid to achieve scale faster and command a better valuation.

To further drive the point home, Arctos published an insightful chart showing the correlation between the distributable fee earnings (DE) multiple and the percentage of Fee paying AUM from traditional Private Equity for publicly listed asset managers.

The trend has driven managers to diversify into private credit and insurance, which has been all the rage recently. But after the BlackRock-GIP deal, which makes BLK the second largest infrastructure investor by AUM, the Private Infrastructure asset class might have turned a corner on its way to become an integral part of investor portfolios.

A Transformative deal

The transaction has the makings of another transformative deal for BlackRock and comes on the back of BlackRock’s ambition to capture share in the high growth asset classes outside the traditional equities and fixed income realm, as it tries to replicate its success in ETFs and active funds at scale in private markets.

“Our acquisition philosophy has always been about growth. With GIP, I truly believe that this will be the case again,” - Larry Fink, BlackRock CEO

Before the deal, BlackRock’s private market assets had ~$50B private Infra. AUM. Post closing it will get 100% of management fee from GIP’s funds and 40% of carried interest from future funds, tripling its current AUM (by adding $106bn of GIPs assets) and doubling the fee revenues.

But its not just about the numbers. GIP has established itself as one of the largest infrastructure investors with a wealth of experience managing and improving hard to operate assets like airports, green energy, pipelines, data centres and the like.

Both Larry Fink and Adebayo Ogunlesi (GIP Chair and CEO) believed that private markets were entering a consolidation phase where size, resources and deep expertise would be needed to get access to the best deals.

“BlackRock and GIP will be able to connect our clients with bigger and better opportunities while also accelerating growth, diversifying revenues and generating earnings for our shareholders” - Larry Fink

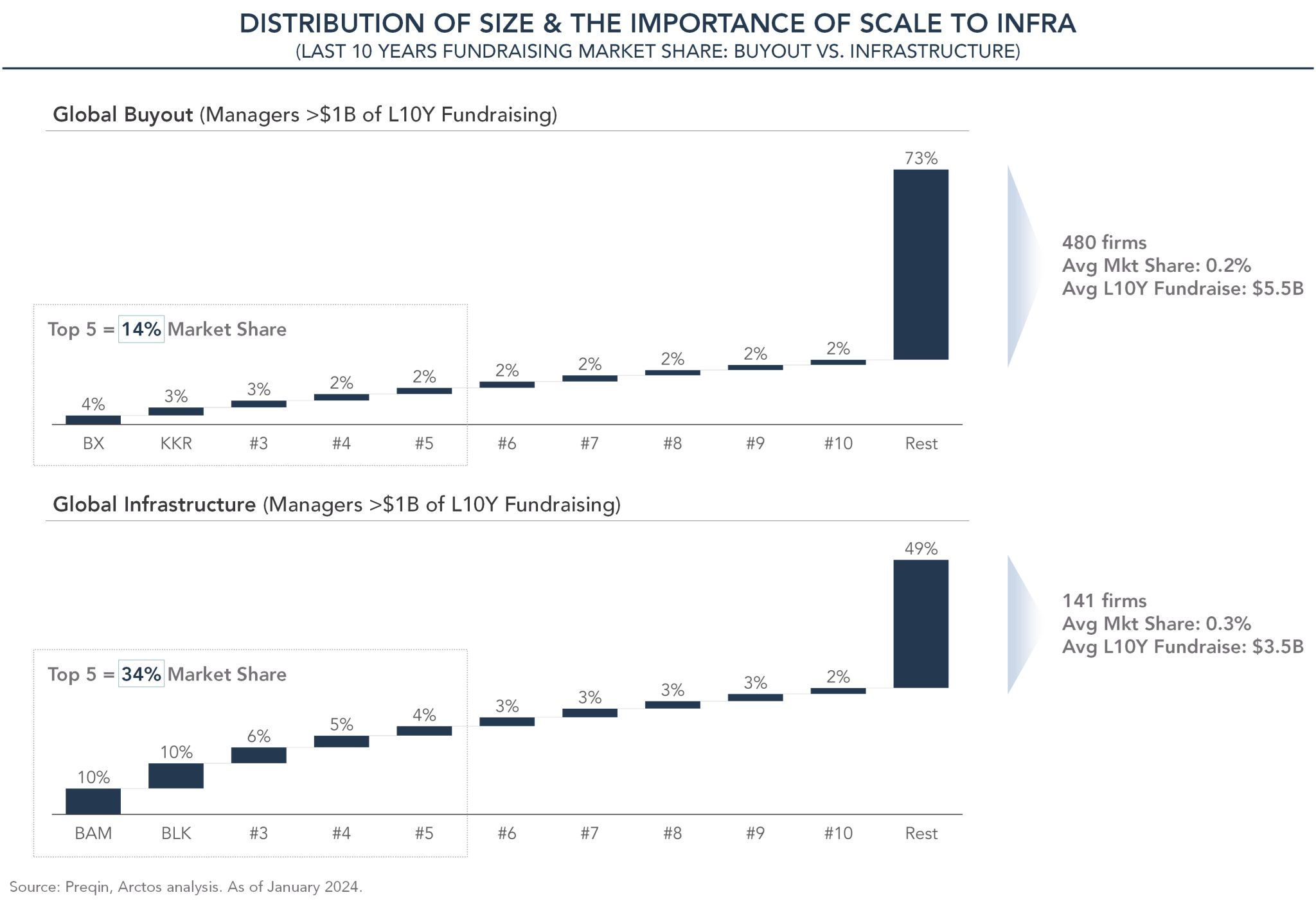

As we’ve mentioned before, scale is everything in asset management. Even more so when it comes to Infrastructure, as this chart from Arctos shows. The top 5 Managers command more than a third of the total AUM raised over the last decade.

BlackRock can use their presence in both retail and institutional channels to now distribute Infrastructure funds unlocking the next phase of growth. On deals where they were competing before, GIP and BlackRock can now combine their resources to win the access and operate these assets.

It was a shared vision of Fink and Ogunlesi, who met first when they both worked at First Boston, that Infrastructure would be the fastest growing part of private markets. There are multiple tailwinds currently helping their vision get closer to becoming reality.

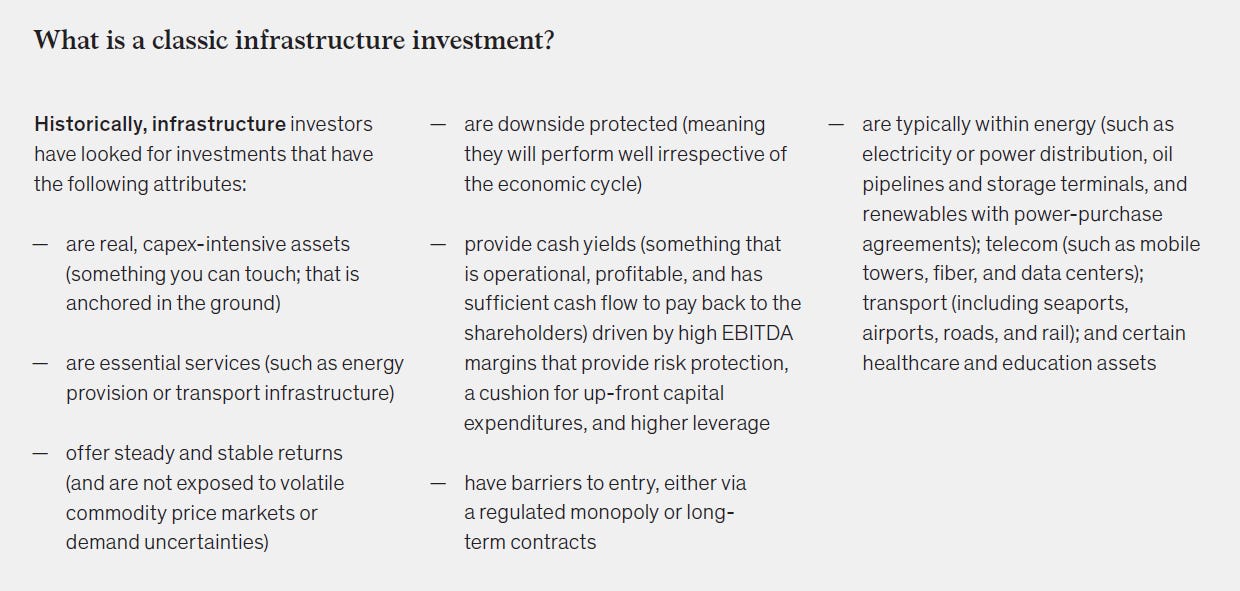

The changing nature of Infrastructure

Infrastructure investing was considered a low risk, stable asset class for a long time delivering predictable returns over a cycle. There was little competition for these assets as access to deals and room for growth was limited. Most large infrastructure assets were publicly owned and operated and are generally highly regulated. More involvement of public entities is an added factor that makes these assets harder to manage. But these challenges slowly started turning into opportunities.

Higher debt burdens: Debt burdens of governments across the world kept climbing higher, restricting their ability and capacity to invest and maintain infrastructure assets.

A large funding gap of trillions of dollars (estimated to be $15T by 2040) has opened up which led to whole or parts of these assets being divested to private investors. Private Capital is now increasingly being preferred for new greenfield infra. projects as well, where pension funds, Private Fund Managers and sovereign wealth funds of countries with surplus cash are stepping up.

Increasing investment needs: New infrastructure assets related to energy transition and green energy, digital infrastructure and supply chains has unlocked a massive amount of capital need and brought it to the forefront.

Decarbonisation: The global economy needs an estimated $9.2 trillion in annual average investment in physical assets (energy transition and green energy generation) to achieve net-zero emissions by 2050, and Europe alone needs almost $2 trillion a year between 2031 and 2050 to meet its targets.

Digital infrastructure and connectivity: The world still needs more high speed connectivity and compute infrastructure in the form of satellite and fibre networks, towers, data centres as we move onto the next technology epoch. Brookfield’s 49% stake in Intel’s new semiconductor chip factory is classic example of how the scope of digital infra. investments is only expanding.

Supply chain resiliency: The global supply chains and trade networks are being reorganised for resiliency and security and the nearshoring/friendshoring tailwind is boosting private investments in manufacturing and transport infrastructure. For example, Mexico and Canada have overtaken China as primary suppliers of goods to the U.S. Nearshoring is expected to bring “billions of dollars of export growth to other LatAm countries, including Argentina ($3.9bn), Colombia ($2.6bn), and Brazil ($7.8bn).” Other regions in Asia are experiencing similar trends.

Active asset management: Infrastructure investments playbooks have been updated to include active management of the business and operations to create more value and increase the return potential. GIP shares an interesting example where it reduced the airport security times at the Gatwick Airport by using bigger trays, so that flyers spend more time in restaurants where the airport owner (GIP) gets concessions on every purchase.

Additionally, these assets have long been natural monopolies which creates sufficiently high barriers to entry making a stronger case for investors to get in first. Being previously owned by governments brings forth new operational value creation opportunities - remove inefficiencies, realign capital and resource allocation towards growth and increase focus on customer service via digitalisation and technology led improvements, amongst others.

The changing nature of infrastructure - from low risk stable asset class to a dynamic higher return potential with more room to actively manage operations to create value is attracting investors to allocate a larger portion of their assets to this asset class.

Private Infrastructure AUM increased at a 20%+ CAGR from 2016 to 2022, crossing the $1 trillion mark. While lack of low cost financing has slowed down fund raising and dealmaking recently, the AUM is still expected to keep growing and cross $1.5T over the next 5 years. Regional funds are inviting the most interest and capital for both sustainable and essential infrastructure investments. Europe presents a better opportunity set, where the AUM is expected to grow at the highest rate in the medium term.

Two recent megacap fund closes - Macquarie $8B European Infra. fund and KKR’s $6.5B Asia Infra fund are clear signs of strength in Real Assets, where the interest in and demand for the asset class is now getting real.

Until next time,

The Atomic Investor