The two types of wealthy (I)

Looking at two types of wealthy via BX's and LVMH's recent quarterly results

Wealth and affluence come in many shapes and forms. Some define it by the number of digits in their bank account balance, some by their tastes and how they consume and live their life, and others by their net worth and how much can they invest.

Different types of wealthy behave differently when conditions change. But if there was anything that rarely changes, it is the willingness to preserve or better the status of their wealth.

This earnings season highlighted two (out of the many) types of wealthy and gave us some timeless insights into their behaviour.

In Part I I look at one of these, the wealthy investor, and see how they are reacting to this new environment.

The wealthy investor - Back in preservation mode

One of the lesser known drivers of Blackstone’s (NYSE: BX) mammoth growth in AUM has been the private wealth or the “retail” channel. About six years ago, the company introduced a whole new team and range of investment products in private equity and private real estate markets for HNW individuals, which has been massively successful in allowing it to tap into an $85 trillion market. In 2022 alone, the private wealth channel brought in $48 billion of inflows (out of 226 billion overall). In Q4, as announced in the recent earnings call, the retail channel allocated $8 billion to BX’s products.

BX’s private real estate fund (BREIT) was up 8% last year as compared to a -25% return in the public REIT index. Equity markets were down between 18-30% and bonds bled trillions of dollars throughout the year. Given lower volatility and long term duration of realisations of returns, the wealthy investor allocated an increasing amount to private markets and funds which were outperforming their public market portfolios.

Earlier in Q3 2022, the BREIT faced a considerable number of redemptions from private investors when interest rates were jacked up and the markets plunged. Some investors were trying to sell-off their BREIT shares (which were still doing quite well) to offset their losses in other parts of the portfolio while others were raising some additional cash for their portfolios.

On the earnings call, the management acknowledged the expected slowdown in fundraising and inflows.

And it's an area that we think can grow quite significantly over time. But in the near term, I think the growth will be a little more muted

The wealthy investor, by the looks of it, is still allocating to parts of the market which are deemed less volatile but is back in wealth preservation mode after multiplying it by manifold in the last decade.

Blackstone’s Q4 - Trickling back to normal

As I mentioned here recently, Blackstone’s success over the last decade has been driven by its ability to raise an increasing amount of funds across its business segments, convert a larger part of its AUM to perpetual vehicles (raise longer-term capital which means longer duration of fee revenues) and increase earnings stability with a higher proportion of it coming through a more stable fee revenue on AUM.

It has unlocked various sources of capital which it can rely upon for for deployment, generate returns and use the performance to attract more inflows. When the cost of capital was low and financing was dirt cheap, institutional investors were increasingly allocating more towards private markets. The wealthy investor was also looking for alternative sources of returns outside the traditional equities and fixed income, some of which could be found here.

But as the market turned and the fear of recession loomed with much higher interest rates, one would naturally expect inflows to slow down for a business like BX after record breaking fundraising years during 2020-21-H122. Not just yet.

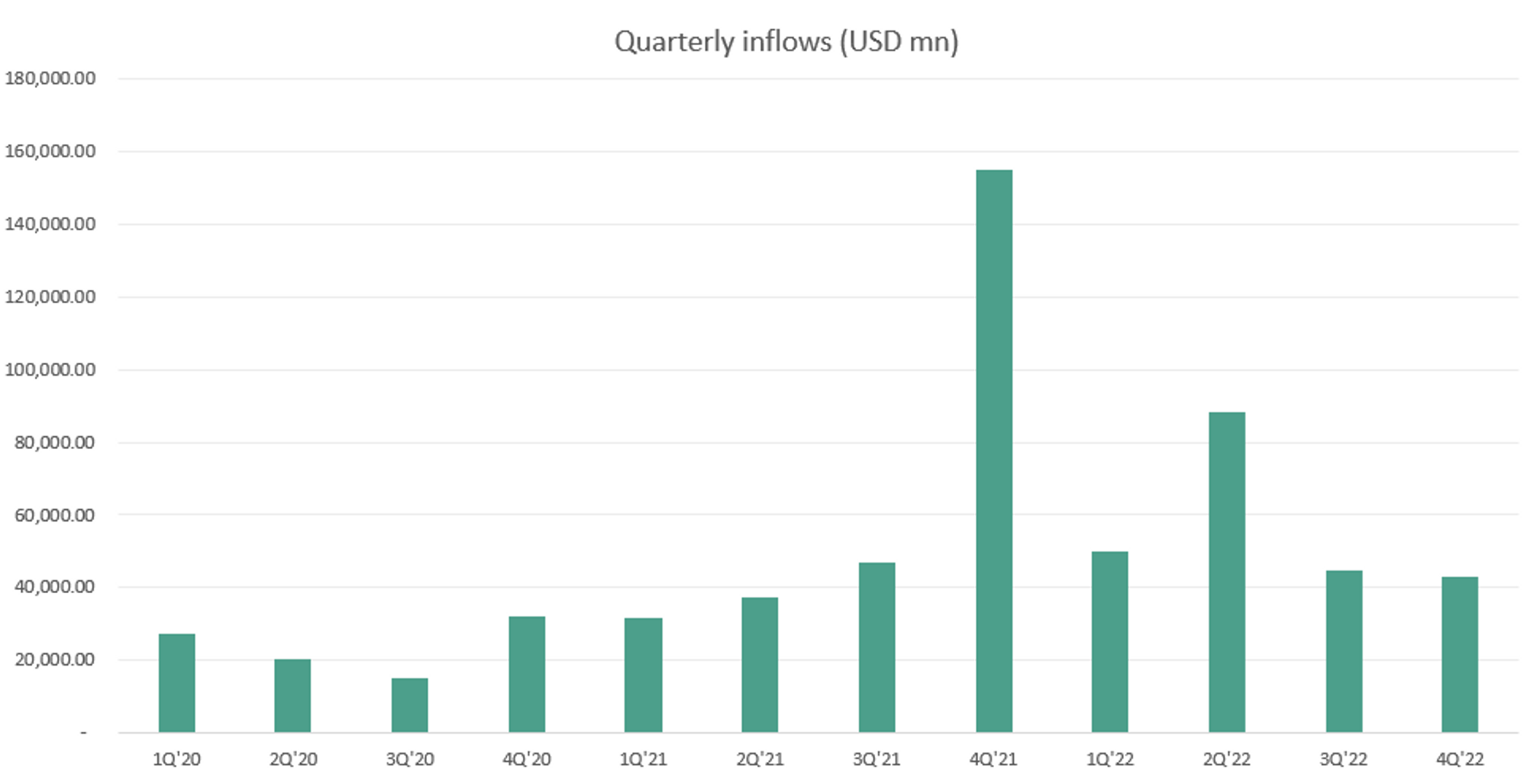

Inflows this quarter were still quite robust at $43bn, taking the 2022 total to 226bn. AUM is now at a record high of $975 billion, up 11% YoY. Fee-generating AUM is now at $718bn while perpetual AUM was up 18% YoY at $371.1bn, now making up more than 32.5% of total AUM.

BX deployed $18.7bn in the quarter and $120bn for the year, and realisations (investment exits) were $13.5bn in the quarter and $81.8bn in the year.

For context - BX raises AUM, earns a management fee, deploys the AUM, realises the investments and takes a performance fee off the realised investment returns.

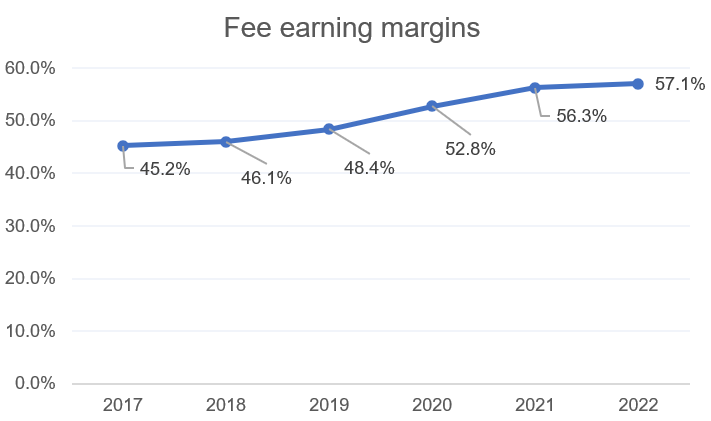

Fee related earnings (Fees - fee expenses) were $1.1bn for the quarter, down from Q4 last year but up for the year at $4.4bn. FRE margins continued to expand and are now at 57.1% (from 56.3% in 2021).

Net realisations (performance fee - compensation) were at $3bn for the year but down more than 60% for the quarter on a YoY basis (less liquidity and higher rates → tighter financing, lower buyouts and falling valuations)

Post-tax distributable earnings (Fee earnings + Net realisations, the cash flow for shareholders) grew to $6.6bn. The DE has a 3 year CAGR of 32%.

BX declared a dividend of $4.4 per share (which has grown at a CAGR of 10% over the last 5 years and 20% over the last decade) and now has returned $1.1bn in the quarter with over $6.1bn in the year. That’s over 90% of its distrubutable earnings returned to shareholders.

The stock is up 32% this year already, but is still down 30-35% from its high.

Valuations are down from its highs too, but it is not as cheap as it was just a few months ago.

Both fundraising and realisations are likely to slow down going forward, which would be a headwind for AUM growth and fees. However, it still has $187bn of dry powder (committed but not invested capital) available for deployments, which might allow it to invest at lower valuations and enhance its future investment returns, and thereby its performance fees.

The management struck a defensive tone during the earnings call realising the macro headwinds and a slowdown in fundraising and investing environment. If it can navigate the outflows from perpetual funds well, the Raise → Deploy → Return → Raise cycle still looks on well on track, albeit with a slower pace of change from one step to the next one.

In the next part of this post, I’ll look at another type of wealthy, the wealthy consumer and how its behaviour has been quite different from the wealthy investor’s.

Until next time,

The Atomic Investor

Amazing srart to the article ocean of knowledge 👍