When the going gets tough

Private Equity firms are getting more creative to get the deals over the line and make sure the PE flywheel keeps rolling.

As the markets leave Q1 behind in the rearview mirror and move deeper into Q2 territory, you start getting a sense of what turn this year might take and if there is a shift in the overall narrative. The protagonists still seem to be inflation and the trajectory of interest rates. The consequent fallout in the economy and asset prices is still casting its shadow on investor sentiment.

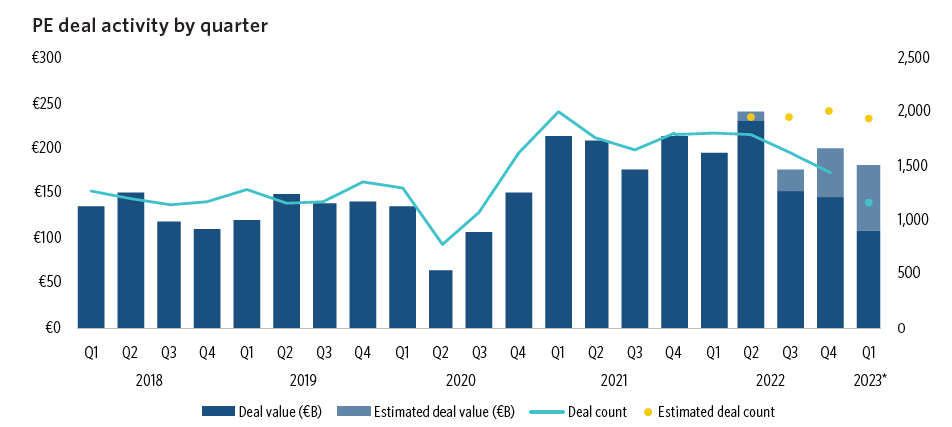

Public markets faced the music last year and everyone’s expecting private markets to go through something similar in this one. The dealmaking environment is torrid, financing is harder to come by and valuations are feeling the effect of gravity after quite some time. Q1 numbers for PE in the U.S and Europe are telling a part of that story.

Now this is a problem. Large fund managers have not pared back on their efforts to raise larger funds in their flagships. On top of that the “dry powder” pile, the funds available for PEs to invest, keeps getting bigger and bigger and has now exceeded the $3 trillion mark.

So the PE flywheel of raise → invest → exit → return capital → raise again stops in its tracks if you cannot move to step 2 i.e invest or deploy capital, get deals done and realise those returns to give your investors back their capital.

On the other hand, one could argue that fund managers could hold onto their portfolio companies for longer, avoid crystallising lower valuations and wait for the market to get better. This is possible but PE managers are always running against the IRR clock. The longer they wait to return capital to LPs, the worse their performance metrics get, which is detrimental to their track records. They want to avoid that to the best of their abilities, which is only reasonable.

Therefore, doing nothing is not a viable option in this environment.

Deploying the capital while navigating this environment and getting deals over the line is where the going is getting tough for PEs. And when the going gets tough…you see some creative options being pulled out of the PE toolkit to keep the flywheel rolling.

Putting more on the line

A typical financing package for a deal is usually comprised of 20-40% equity and 60-70% debt, depending upon the sector and the size of the deal. A tougher financing environment has made it tough for PEs to fund large deals using debt. Banks are not willing to take that level of risk given where rates are and what the banking sector is going through. Private credit funds have stepped in to take some of that share, but there is a limit to the size of financing package they can arrange, along with being more expensive and covenant heavy providers of debt capital.

To counter this, PEs been putting up more on the line and upping their stakes . Some of the deals that have been struck recently are seeing, on average, an equity component of as high as 70%. Silverlake buying out Qualtrics for $12bn with $10bn of equity is an extreme, but a notable example of that nonetheless.

Adding on

While larger deals are increasingly getting harder to get over the line, PEs have shifted towards add-on type deals - buying a smaller target for an existing platform portfolio company. They accounted for a total of 48% of deals in Q1 this year in the U.S.

When valuations are falling and hitting your unrealised returns, these deals are like a band-aid measure to grow the revenue and EBITDA of your portfolio company and make up for some of those lost returns. Lower multiples also mean they can get these done on the cheap and a lot more easily given the size of the deal.

Alternative sources of financing

PE firms have been using alternative sources of capital to close the funding gap like NAV loans and Sellers notes.

Net Asset Value (NAV) loans, which allow firms to borrow against the value of their fund’s overall portfolio, have been increasing in popularity. According to Pitchbook, deal volume in NAV loans increased 50% in 2022 and the market is expected to reach $300bn by 2025.

Seller note is a type of debt in which the seller agrees to receive the purchase value as a series of debt payments, allowing the buyer to add another component to the financing package and close the funding gap. Recently, Emerson Electric sold a majority stake in its climate technologies unit to Blackstone for $14bn, which included a $2.25bn 10-year seller note provided by Emerson itself at 5% interest.

Earnout provisions

To get transactions done, buyers are now including earnout provisions that allow them to defer a portion of the purchase price and make those payments when the target meets certain milestones like an absolute EBITDA level or a critical development like a regulatory approval.

This ensures that the buyers get the deal over the line and avoid paying a hefty price unless the company reaches the targets it is promising during the sale. It also reduces some uncertainty around the company’s future performance (that is usually baked into the asking price) and aligns the management to deliver better on the promised performance targets.

In 2022, 21% of M&A deals included these provisions, up from 17% in 2021.

Liquid exits

Exits are as important as deploying capital as they allow investment managers to return cash back to their LPs and realise the returns for the fund. In a year where exiting at a valuation you want is not going to be easy, fund managers are looking at other ways to generate liquidity like selling minority stakes, setting up continuation vehicles and creating semi-liquid funds.

Minority stake sales are a tried and tested lever to pull to cash out on some the unrealised returns by selling a stake in the company to another PE player or an investor and return some of the cash back to LPs.

Continuation vehicles are increasingly becoming popular, where funds would sell the company to the next vintage of the same fund to generate enough liquidity for the LPs of the existing fund. This also allows PEs to hold on to business with a larger growth potential for far longer.

Semi-liquid funds are being offered to the “retail’ segment of the PE market i.e the HNW individuals or groups investing in private markets. Firms like Blackstone and KKR offer funds where investors can request redemptions like in a public markets mutual fund (capped to a certain % of the fund’s assets) which they cannot do in a traditional closed end PE fund. EQT, the Swedish PE fund manager, mentioned on its recent earnings call that it also plans to launch a similar fund offering this year, which goes to show how it could become increasingly popular going forward.

Portable leverage

Portable capital structures, where the existing debt of the target company is kept on the balance sheet instead of refinancing it completely, is being preferred by a meaningful number of buyers and investment banks involved in the deal. The reason is simple. Interest rates are substantially higher and it is a lot more expensive to get new debt in place.

Buyers, therefore, are trying to structure the transaction in a way that it does not trigger a change of control of ownership, which would mean the existing debt would have to be repaid. Brookfield’s sale of Westinghouse was the one where its existing $3.4bn debt stayed in place as Brookfield only sold a minority stake. Partners Group’s sale of a 50% stake in USIC to KKR is another example where no new debt was raised. An intelligent way to sidestep the credit markets if you can manage to pull it off.

Private markets may be going through a tough time but it seems like doing nothing is not an option PEs would like to choose. The PE flywheel needs to keep rolling even when the going gets tough, and now they have the tools to be able to ride this tough market environment for longer.

Until next time,

The Atomic Investor

PE# the trending topic # your genetic touch @ atomic investor